Friend of the Hound and all around damn smart dude, Credo, will be contributing here to ESG Hound from time to time. He’s probably the best off the wall microcap ideas guy I’ve ever known and a wizard at charts and flows and finance. He’ll be focusing on small caps with big potential and an ESG bent.

Vidler Water Resources Q&A Session

So as Predicted, a Tier 1 water shortage was declared for Lake Mead yesterday, 8/16/2021.

I was inspired to look into Vidler Water Resources (Ticker: VWTR) from friend of the ‘stack, and now ESG Hound contributor Credo. He wrote the original 100 page long (and brilliant) VWTR manifesto, which you can find by clicking HERE. I followed that up by talking about the ethical ESG case for buying water rights HERE.

Credo got a ton of questions about the original tome and he assembled them into a lengthy Q&A which I’ve posted as a pdf below.

So, you asked and we (well, Credo) answered. I’ve made an abridged version of the Q&A below, edited for brevity. In the full version he talks bitcoin, twitter beefs, commentary on VWTR management statements, stock price volatility, and compares VWTR to a Florida property management company.

Q: Can you give us a little background on yourself and how you became interested in this topic?

Credo: Just for disclosure, I’m not an expert in the field of hydrology, meteorology, climatology or any of the other -ogies that a reader would assume what I write should be relied upon with any semblance of expert advice. I encourage everyone to do their own research and I think the discussion around what the West is facing related to this drought is a step in the right direction. One of the things I love about this Country (being an immigrant here) is the ability to have access to many sources of information and the opportunity to discuss openly if you disagree. It is by far one of the most underrated benefits if you’ve seen the complete opposite.

Q: Why is this such a controversial topic?

And of course, as I suggested in the original piece, this topic is just political tinder. (…) It’s just the type of topic that unfortunately has a party affiliation bias and that’s not productive. I live in Texas and my father lives in California; when the winter storm in Texas happened, he was worried about me and when I hear about blackouts and potential impacts of this epic drought, I worry about him. There’s a human element/aspect to what’s going on that is much more important than the politicized angle, especially after the last 18 months many have endured.

Q: It’s hard to think about water as a commodity. It doesn’t have much price history, dependent on geography and you can’t take delivery of it. Why do you think that will change?

Good question, “lots to unpack” there.

I believe water is just in the infancy stage of being treated as a commodity. All the points you make are true and with the potential exception of taking delivery (which I think would be poor policy), I believe most other characteristics that other commodities exhibit, water already exhibits and if there was push forward to have market pricing specific to each state, it could potentially act as better public policy (I haven’t made up my mind on water market pricing as good public policy yet). I understand the unintended consequences related to financializing a Maslow’s Hierarchy of Need commodity might be considered political suicide, but I also think we’re very close to Crossing the Rubicon if we don’t. Because it’s not just one Maslow’s Hierarchy of Need, not having secure source of water impacts all the Physiological Needs (food, water, shelter, etc.).

Q: And commodity delivery?

Regarding taking delivery. There are other commodities that you don’t take delivery of and have contracts. The most basic is WTI contracts are delivery, Brent aren’t. The one I have the most experience with that you can’t take delivery of is uranium and there are very good reasons for that (thankfully).

For one, the uranium market has a primary and secondary supply mechanism. The primary source is driven by mining and that’s controlled by two large players and the secondary source is from stocks, Mox & Repu, tails and heu. The primary source is always at risk and the demand is very consistent because there is a big lag between when yellow cake is mined to when it is used as fuel in a reactor. The secondary source exhibits a very fickle behavior. You would think that when primary supply is impacted by any sort of disruption that secondary source would cover the shortfall, but that’s not always the case. In fact, it’s the secondary source that recently exhibited supply tightness before primary source did. How this relates to water as a commodity is the primary source of water is today at risk and water is the type of commodity where the moment it exhibits tightness, the secondary source will soon follow.

Q: What makes Arizona so special in regards to water rights?

In Arizona and Nevada these dynamics are very much in play. Arizona has a sizable “top 10%” population and a growing tech/ESG/EV presence and this demand is not very price sensitive. For Taiwan Semiconductor/Intel and the other semi’s that have announced plans to expand or have built a presence in the last three years, water as a percentage of total operating expenses is de minimis and that automatically increases career risk. The top 20% of golf courses, solar projects, TenWest Link, you name it, there’s an existing and growing demand for water in Arizona with inelastic demand and that is very important to understand. The population growth has been underestimated in this region and the model hasn’t been quick to adjust for population, weather change and growing tech presence. It’s a failure of capturing small changes over a long period of time and when/if you have a 1 in 1,000-year drought all the other aspects in the model are questioned and you have an IV blowout. I touched on how insurance companies are thinking about some of these 1 in 1,000-year events, the models are being questioned and when you experience losses in insurance/credit, the price discovery of insurance premiums / cost to finance operations impacted by climate change (electricity, food, business interruption, etc.).

The geographic dependency on supply as an attribute is much stronger with water. For uranium, US DoD demand needs to be sourced domestically from the US and I’m not going to dive into Section 232. For water, there’s existing geographic infrastructure that serves provides water supplies that requires years of approval/permitting/ construction to adjust, and the West is simply not prepared to make long term decisions in a very short period. There’s a reason why the NQH2O Veles Water contract is up 80%+ YTD, it’s the only form of daily price for water and that strong supports the idea of water as a commodity undergoing price discovery. Further, the 80%+ move has been without financialization as the WWTR trust (trust created to purchase NQH2O) is still in SEC prospectus status.

From a geographic standpoint, there’s a migration “tax arbitrage” that serves as a tailwind for Nevada and Arizona. The existing tax and incremental taxes the state of California continues to implement on what appears to be an already heavy individual/corporate tax burden leads to migration out of California to Arizona and Nevada. It increases future demand for water and since Arizona has the most junior rights from Lake Mead and carry the heaviest burden from the decline in water levels at Lake Mead, Arizona is unique.

Q: Can you go a bit more into how the LTSCs work and what makes them challenging to value?

Specific to Vidler Water Resources Inc, the long-term storage credits (“LTSC”) exhibit the closest “spot market” pricing for water and LTSCs apply to Arizona. It’s also a secondary source of supply that undergoes tightness when the primary source is tight. Because LTSC creation is largely driven by excess supply from primary source. This is another rabbit hole; in Arizona there are certain groups that have been overallocated water based on right of use. For many years, Native American tribes/farmers were allocated water and (still do, to this day), because they didn’t have 100% demand for the water that was allocated to them, LTSCs served as a way to monetize that extra water and depositing water in exchange for LTSCs that were then sold to other users that needed water. This is where I believe Arizona was very innovative. Now a lot of these groups that monetized their LTSCs, what they did with the proceeds is what makes this interesting. After monetizing LTSCs, many then used proceeds to purchase real estate (multi family, commercial, etc.), diversify into farming and other ventures that increases future require water. They also saw the models and likely thought “we get X% of excess water and that will continue because we are entitled and diversifying source of revenue lowers business risk, so why not?

Q: How do current LTSC prices relate to prices of LTSCs in VWTR’s Portfolio?

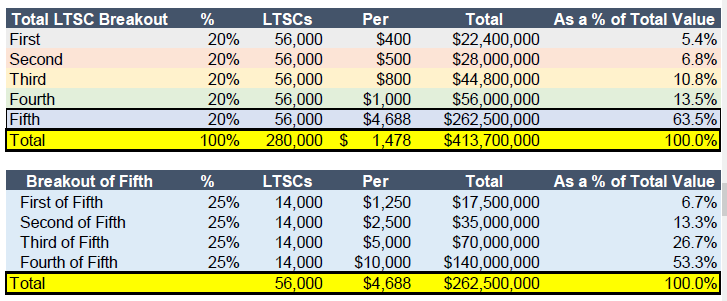

As it relates to LTSCs, using one price for all the LTSCs is bonkers. If you think all the LTSCs should be valued at one price, then how was Vidler able to sell 2,000 of their Arizona LTSCs for $1,630/per earlier this year? I see various comments and feedback that values all the LTSCs at same value as if Vidler with their 280,000 LTSC would today sell all of their LTSCs at $400 each and that assumption requires one to assume the first 1/5th of LTSCs sold has the same value as the last 1/5th. It doesn’t. Here’s a very simple way of thinking about it and I just put these numbers together for illustration, in the original report I did hint that I can made this work if I started with $150 as base for LTSCs because the right way to think about LTSC pricing is to think about inelastic demand and convexity.

I challenge you to go to VWTR and tell them you want to buy all their LTSCs at average price of $350, they will likely chuckle, hang up, then that chuckle will turn into full cackle. Because they’ve hinted at this (I’ll expand). The above table assumes you have 280,000 LTSCs, my model I use has many different levers to it (this is just for illustration, I literally just opened up excel and didn’t want to spend more than three minutes), but let’s assume you sell them in 1/5th tranches and the last 1/5th is sold in 1/4th tranches. It is more likely each 1/5th has their own 1/5th to 1/10th because selling 50,000 LTSCs when the LTSC supply is not growing is different than selling 50,000 LTSCs when there wasn’t a tier 1 shortage in place for the following calendar year and supply of LTSCs was much higher.

Q: Why shouldn’t an outsider just take the current market LTSC price, multiply it by VWTRs holdings and call it a day for a rough valuation?

So, you want to be the guy that uses $300-$400 on all the LTSCs to assign a value, I want you to know you’re wrong. 1. The $300-$400 price is what was being referenced in 2016-2017, 2. That’s not how the remaining LTSCs will be sold. If they are, I will gracefully admit I’m wrong, but I think I’ve done sufficient due diligence that suggest my way of valuing the LTSCs is the way to go vs. the “I’m just going to take total number of LTSCs and one price” route. Time will tell (“TWT”), it always does.

Q: I didn’t see how you came up with the valuation and I’m not getting to your $25-$50 price.

Oliver Wendell Holmes once said, “The right to swing my fist ends where the other man's nose begins" and my response to this question is “my right to swing at your price ends when I see your LTSC pricing model.”

Let’s start with the most basic calculation and answer a “few” basic questions:

Do you believe that in the last three years, the assets VWTR owns have increased in value? Because I do. I think they have been conservatively rising by at least 5% semi-annually.

Do you believe the Company’s cash burn today vs. three years ago and the ability to shield taxable income in an environment that many people believe we’ll experience higher tax rates is an improvement?

Do you think a tier 1 shortage declaration which hasn’t gone into effect and won’t go into effect until 1/1/22 will likely change the behavior of buyers that require water supplies and therefore could likely increase the value/timing of monetization of assets?

If the answer to any of those three questions from a starting point of 7/30/18 when the market cap was $20m higher is a no, then I think you should move on to the next idea. Because if we can’t agree on these simple questions, forget about thinking how to value FSR or LTSCs, growing recurring revenue and water “price discovery”. I’ll save you time.

Q: Lake Mead has been flat the last month, any concern?

Not at all, if anything it strengthens the argument these structural issues are more serious than benign. Arizona received more rain in one month during this monsoon season than all of 2020 and that entire region was wet. Yet, Lake Mead stayed flat? The infrastructure is outdated, one month of heavy rain in 2021 doesn’t have the same impact last year or the year before. Population growth in Arizona and Nevada is going through so many regional changes and those attributes don’t translate well into a model that is antiquated. I guess one way to think about it is, would you depend the same vol model in 2010 that you depended on in 2007? Would you trust that model? Probably not, because 1) you will have recency bias, 2) you now have a job because the guy that was depending on the 2007 model in 2008 got laid off and so now you think about your own “career risk” and 3) life is too short. Using the USBR model to make decisions in 2022 after a 1 in 1,000-year drought event they completely missed is a sanity check.

Q: Dude, you know you could have just done a meme and saved a lot of time, right? That’s what I would have done.

How dare you desecrate my version of the Sistine Chapel? Challenge accepted.

It was just three weeks ago I heard some horrible news. The kind you question your place in this world, meaning of life, you name it. Couldn’t believe there was going to be another Waterworld movie. I called my mom and said, “I don’t want to live in a world where Hollywood thinks making a second Waterworld movie is rationale. I can’t do it.”

editor note: Credo may run circles around me on finance, but his meme game needs work

Is Chamath in?

As postulated in my original piece, Chamath’s Social Capital analysts think it’s a good play.

So what's next for this drought play? Let’s wait and see.

Regards,

ESG Hound

Disclosure: The author/editor of this newsletter does not have any position in VWTR. ESG Hound contributor Credo does currently hold long positions in VWTR.